Uninsured vs. Underinsured Motorist Coverage: What’s the Difference and When Does It Apply?

Published: March 12, 2026 · Last updated: March 12, 2026

TL;DR: Uninsured motorist (UM) coverage pays when the at-fault driver has no insurance at all. Underinsured motorist (UIM) coverage pays when the at-fault driver has insurance, but not enough to cover your damages. Both apply to hit-and-run accidents. They are among the most valuable coverages you can carry, and among the most commonly misunderstood. This guide explains how each one works, what states require, and how to use them after an accident.

You were hit by someone who had no insurance. Or they had insurance, but their $25,000 limit covers less than half your hospital bill. What happens now?

This is where your own uninsured and underinsured motorist coverage comes in. Most drivers carry these coverages without fully understanding what they do or when they trigger. This guide explains the mechanics clearly (state by state where it matters), so you know exactly what protection you have and what to do if you need to use it.

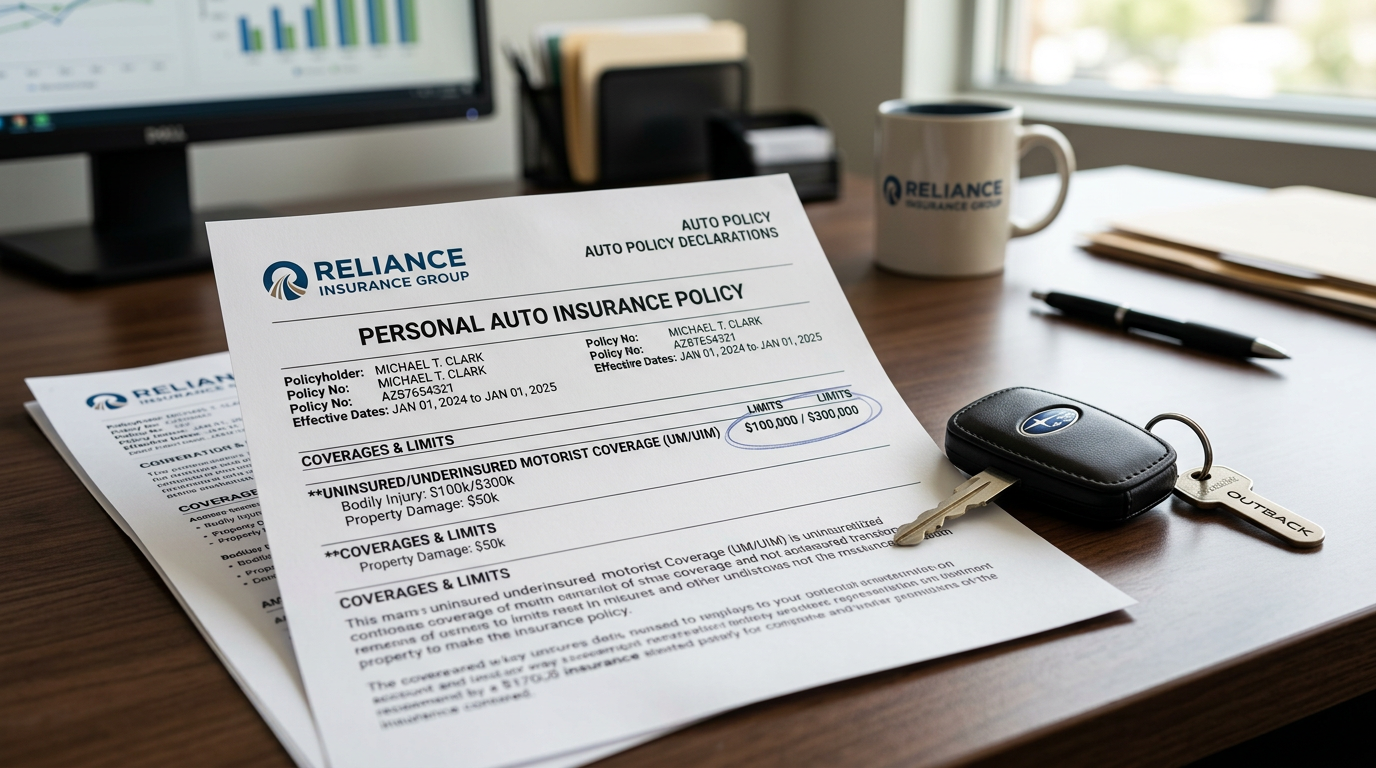

What Is Uninsured Motorist (UM) Coverage?

Uninsured motorist coverage pays for your injuries and damages when the at-fault driver has no auto liability insurance. It steps into the role the other driver’s insurance should have played, covering your medical expenses, lost wages, and pain and suffering up to your UM policy limit.

UM coverage applies in these scenarios:

- The at-fault driver has no liability insurance at all

- The at-fault driver is unidentified (hit-and-run), subject to state-specific requirements

- The at-fault driver’s insurance company denies the claim or becomes insolvent

UM coverage typically pays:

- Medical expenses

- Lost wages

- Pain and suffering

- In many states, property damage (UMPD, or “uninsured motorist property damage,” sometimes a separate coverage option)

What Is Underinsured Motorist (UIM) Coverage?

Underinsured motorist coverage pays when the at-fault driver has insurance, but their policy limits are not enough to fully compensate you for your damages.

Example: You sustain $120,000 in damages. The at-fault driver carries the state minimum of $25,000 per person in liability coverage. Their insurer pays $25,000 to settle the claim. You then make a UIM claim against your own policy. If your UIM limit is $100,000, your insurer pays up to $75,000 more (the gap between the other driver’s $25,000 and your $100,000 UIM limit, though the exact mechanics vary by state).

Why this matters: State minimum liability limits are frequently inadequate for serious injuries. A single emergency room visit and one surgery can easily exceed $50,000. A serious spinal injury can exceed $200,000. If the other driver only carries minimum coverage, UIM coverage is often the only way to be fully compensated.

UM vs. UIM: The Key Distinctions

| Uninsured Motorist (UM) | Underinsured Motorist (UIM) | |

|---|---|---|

| When it applies | At-fault driver has no insurance | At-fault driver has insurance, but limits are too low |

| Hit-and-run | Yes (usually, with police report) | No (UIM requires an identified, insured driver) |

| Who pays your claim | Your own insurer | Your own insurer |

| Trigger | Other driver uninsured | Other driver’s limits < your damages |

| Policy limit | Your UM limit | Your UIM limit (minus what other driver paid) |

In most states, UM and UIM are sold together as a combined coverage, but the triggers and mechanics are distinct.

Is UM/UIM Coverage Required?

This varies significantly by state. Here’s the breakdown:

States where UM coverage is mandatory: Connecticut, Illinois, Kansas, Maine, Maryland, Massachusetts, Minnesota, Missouri, Nebraska, New Hampshire, New Jersey, New York, North Carolina, North Dakota, Oregon, South Carolina, South Dakota, Vermont, Virginia, West Virginia, Wisconsin, and Washington D.C.

States where UM coverage is required to be offered but can be rejected in writing: Alabama, Alaska, Arizona, Arkansas, California, Colorado, Delaware, Florida, Georgia, Hawaii, Idaho, Indiana, Iowa, Kentucky, Louisiana, Michigan, Mississippi, Montana, Nevada, New Mexico, Ohio, Oklahoma, Pennsylvania, Rhode Island, Tennessee, Texas, Utah, Washington, Wyoming, and others.

No-fault states: In states with mandatory personal injury protection (PIP), including Florida, Michigan, New York, New Jersey, Pennsylvania, Hawaii, Kansas, Kentucky, Massachusetts, Minnesota, North Dakota, and Utah, your own PIP coverage pays first for medical expenses. UM/UIM coverage still applies but coordinates with PIP and typically handles damages that exceed PIP limits, including pain and suffering (subject to each state’s tort threshold).

If you waived UM/UIM coverage in writing, you may not have it. Check your declarations page (the first page of your policy) to see what coverages you carry and what limits.

How UIM Claims Work in Practice

UIM claims are more complex than UM claims because they involve two insurers: the at-fault driver’s insurer and your own.

Step 1: Settle with the at-fault driver’s insurer (or exhaust their policy limit). In most states, you must obtain the at-fault driver’s policy limit before your UIM coverage can be triggered.

Step 2: Notify your own insurer of the potential UIM claim before you settle with the at-fault driver. Most policies require this, and some insurers have the right to “step in” and pay the at-fault driver’s limits themselves in order to protect their subrogation rights.

Step 3: File a UIM claim with your own insurer for the remaining damages. Your insurer will evaluate your total damages and apply a credit for what the at-fault driver’s insurer paid.

Step 4: Negotiate or arbitrate. If your insurer disputes your damages or offers less than you believe you’re owed, you typically have the right to negotiate, demand arbitration (required by most policies), or in some states, sue your own insurer for bad faith.

Important: Some states use a “gap” method for UIM (your UIM limit minus the other driver’s limit) and some use a “limits” method (your UIM limit is the total available, with a credit for what was paid). This distinction significantly affects how much coverage is available. An attorney can explain which method applies in your state.

Stacking vs. Non-Stacking

If you insure multiple vehicles on the same policy or have multiple policies, some states allow stacking: adding together the UM/UIM limits from each vehicle to create a larger total coverage pool.

Example: You have two vehicles on one policy, each with $50,000 in UM coverage. In a stacking state, you may have $100,000 available for a UM claim.

States that allow stacking: Florida, Georgia, Missouri, North Dakota, Ohio, Pennsylvania (anti-stacking clauses are sometimes unenforceable), and others.

States that prohibit or restrict stacking: California, Illinois, Indiana, New Jersey, New York, and others.

If you have multiple vehicles, ask your insurer whether stacking is permitted in your state and whether your policy allows it.

The Uninsured Driver Problem Is Real

Approximately 1 in 8 drivers on U.S. roads is uninsured, according to the Insurance Research Council (about 12.6% of motorists nationally). Some states are significantly higher: Mississippi leads at approximately 29.4% of drivers uninsured, followed by Michigan at 25.5%, Tennessee at 23.7%, New Mexico at 21.8%, and Washington at 21.7%.

Even in states with mandatory insurance, enforcement is imperfect. Policies lapse, coverage is canceled for non-payment, and some drivers simply ignore the requirement.

This is why UM coverage is not a premium line item to cut to save money on your policy. If you’re in one of the states above with high uninsured driver rates, the statistical chance of being hit by an uninsured driver is substantial.

What to Do After Being Hit by an Uninsured or Underinsured Driver

- Document the scene as you would any accident: photos, witness information, police report.

- Get the other driver’s insurance information. If they claim to have no insurance, get their name, contact, and driver’s license number anyway.

- File a police report. Required for most hit-and-run UM claims and strongly advisable for all UM/UIM claims.

- Contact your own insurer promptly. Most policies require notice within a reasonable time. Do not delay.

- Do not agree to release any claims against the at-fault driver without your UIM insurer’s consent. Doing so can forfeit your UIM rights.

- Consult an attorney before agreeing to any settlement, especially from your own insurer. UM/UIM claims against your own company can be contentious, and insurers do not always value claims fairly.

Frequently Asked Questions

Does UM coverage apply to accidents where I was a pedestrian or cyclist?

Yes, in most states. UM coverage typically covers you as a named insured regardless of whether you were in a vehicle at the time of the accident. If you were hit by an uninsured driver while walking or cycling, your UM coverage usually applies. Check your policy language and your state’s rules.

Can my own insurer deny a UM/UIM claim?

Yes. Your own insurer can dispute the claim, dispute causation, dispute the value of your injuries, or argue that their policy doesn’t cover the specific circumstances. This is more common than people expect. An insurer denying or underpaying your UM/UIM claim may be acting in bad faith, which creates a separate legal claim in many states.

What happens if my UM/UIM limits aren’t enough either?

If both the at-fault driver’s coverage and your own UM/UIM coverage are exhausted, your remaining options include: pursuing a judgment against the at-fault driver personally (only practical if they have significant assets), umbrella insurance coverage (if you carry it), and in some states, additional excess UM layers. This is the scenario where the coverage decisions made before the accident matter most.

Will filing a UM/UIM claim raise my rates?

It depends on your state and insurer. Some states prohibit insurers from surcharging policyholders for UM/UIM claims where they were not at fault. Others allow it. Check your state’s rules and your policy’s surcharge terms before filing, especially for smaller claims.

The Bottom Line

UM and UIM coverage are among the most important protections you carry. They exist precisely because not every driver on the road is adequately insured, and without them, a serious accident caused by an uninsured or minimally insured driver can leave you absorbing costs that should be someone else’s responsibility.

To start a UM or UIM claim or to connect with a participating attorney who handles these cases, see our UM/UIM case review page.

If you’re dealing with an uninsured or underinsured driver after an accident, get a free case review to understand what coverage is available to you and how to maximize your recovery.

Related guides: